![]()

|

|

|

Chapter 2.4® - How Are Bonds Issue? How do you Trade Bonds? Bond Premiums & Discounts - Contract Rate versus Market Rates

How Bonds are Issued Before the bonds are issued to the public, an issuing organization’s Board of Directors and shareholders must provide a unanimous approval. Bonds are regulated by the Securities Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA). Registration with the SEC requires stating the number of bonds authorized to be issued, par value, contract interest rate, when interest payments are to be made, and other relevant information. Bonds are usually offered in denominations of $1000 or $5000. The legal document that states the rights and obligations of bondholders and issuers is known as a Bond Indenture. The issuing company usually sells the bonds to an investment firm such as Goldman Sachs or TD Waterhouse, also known as an Underwriter. The underwriters then sell the bonds to the investment public & other investment organizations. The rights of the bondholders are administered and protected by a Bond Trustee whose function is to represent the bondholders in the event of a default. Other functions that a bond Trustee does is:

Trading Bonds The sale or offering of bonds to general investment public is called floating an issue. Since bonds are traded on the market, they have a market value or price. Thus, bond market values are expressed as a percent of their face value (par value). For instance, an organization’s bonds might be trading at 105 and ½ meaning they can be bought for 105.50% of their par value. Bonds that trade above their market value trade at a premium. Bonds that trade below market value trade at a discount. Thus, bonds that trade at 105 and ½ are trading at a premium, while bonds that are trading at 97 and ¼ are trading at a discount. The market rate of interest (effective interest rate) is the % of interest borrowers are willing to pay and lenders are willing to earn for a certain bond taking in to account its risk level. When the bond contract rate equals the market effective interest rate, the bond trades at par value or 100%. When the contract rate does not equal effective interest rate, the bond trades above or below par value; the summary is shown in the table below. Bond Premiums & Discounts - Contract Rate versus Market Rates

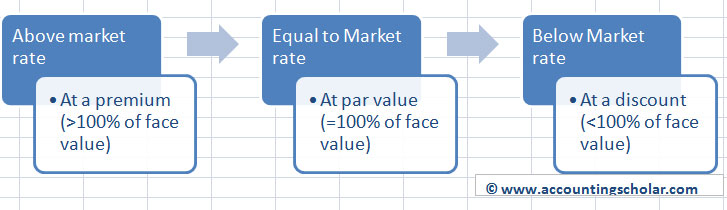

This graph shows the effects of market rate

being greater than the contract rate, less than the contract rate or equal

to the contract rate. If the contract rate is greater than the market

rate, then the bond is issued at a premium (>100% of face value). If

the contract rate is equal to market rate, then the bond is issued at

par value (=100% of face value). And lastly if the contract rate is below

market rate, then the bond is issued at a discount (<100% of face value). |

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |